You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Which Medicare Advantage Plan will you be choosing for 2025 & Why?

- Thread starter Vanessa2U

- Start date

Happyflowerlady

Vagabond Flowerchild

- Location

- Northern Alabama

We moved from Humana to Devoted Health last year, after a recommendation from our medicare insurance broker, who went over the plans with us a year ago. He recommended Devoted because they are a Five Star company, and both the doctors and the patients liked the company and recommended it. They have exceptionally good extra benefits.

Last year was the first year in Alabama for Devoted, so it is still pretty new, even this year, but growing.

Our hospital system just announced that they are having some kind of irreconcilable differences with United Health Care (the one recommended by AARP), so none of the doctors or facilities who belong to the HHS will be accepting UHC insurance next year. I do not know if other parts of the country are having the same issues with UHC or if it is just our hospital, but in any case, a lot of people here depend on the Huntsville hospital and its doctors, so people will be changing from UHC to some other plan.

Last year was the first year in Alabama for Devoted, so it is still pretty new, even this year, but growing.

Our hospital system just announced that they are having some kind of irreconcilable differences with United Health Care (the one recommended by AARP), so none of the doctors or facilities who belong to the HHS will be accepting UHC insurance next year. I do not know if other parts of the country are having the same issues with UHC or if it is just our hospital, but in any case, a lot of people here depend on the Huntsville hospital and its doctors, so people will be changing from UHC to some other plan.

Vanessa2U

New Member

Devoted Health isn't in my area yet. Thanks!We moved from Humana to Devoted Health last year, after a recommendation from our medicare insurance broker, who went over the plans with us a year ago. He recommended Devoted because they are a Five Star company, and both the doctors and the patients liked the company and recommended it. They have exceptionally good extra benefits.

Last year was the first year in Alabama for Devoted, so it is still pretty new, even this year, but growing.

Our hospital system just announced that they are having some kind of irreconcilable differences with United Health Care (the one recommended by AARP), so none of the doctors or facilities who belong to the HHS will be accepting UHC insurance next year. I do not know if other parts of the country are having the same issues with UHC or if it is just our hospital, but in any case, a lot of people here depend on the Huntsville hospital and its doctors, so people will be changing from UHC to some other plan.

David777

Well-known Member

- Location

- Silicon Valley

Another mostly healthy person that has been fine with current plans so avoids switching. Have had KP since retiring in 2017 and before that while employed since 2010 KP also. My 4 top rated KP doctors treat me as one of significant public importance. There is a large new modern KP hospital with highest level facilities just a few miles drive that as a senior, does provide reasons to continue living here versus say moving to some smaller city. Also offices just a mile away where next Tuesday for example will walk-in without an appointment for free flu and COVID-19 vaccinations.

Last edited:

Vanessa2U

New Member

What does KP stand for?Another mostly healthy person that has been fine with current plans so avoids switching. Have had KP since retiring in 2017 and before that while employed since 2010 KP also. My 4 top rated KP doctors treat me as one of significant public importance. There is a large new modern KP hospital with highest level facilities just a few miles drive that as a senior, does provide reasons to continue living here versus say moving to some smaller city. Also offices just a mile away where next Tuesday for example will walk-in without an appointment for free flu and COVID-19 vaccinations.

Llynn

Non-ranked Constituent

- Location

- Pacific NorthWET

Kaiser PermenentieWhat does KP stand for?

Because I'm in the midst of cancer treatment, I will be staying with them in 2025.

Mr. Ed

Be what you is not what you what you ain’t

- Location

- Central NY

You are absolutely right. Stick with Medicare.None. Medicare Advantage Plans are a scam. I'll never leave original Medicare.

stretch5881

Member

- Location

- Wisconsin

Original Medicare with a G supplement plan. It costs more up front, but pays to have it when you need it.

Advantage plans are low cost up front, but have high deductibles. Many of the costs related to an illness are not covered by the plans and don't go toward the deductible either.

Some care facilities won't accept patients with advantage plans because of the negotiated prices.

Either way you choose, it will cost you. In premium prices, or out of pocket.

Advantage plans are low cost up front, but have high deductibles. Many of the costs related to an illness are not covered by the plans and don't go toward the deductible either.

Some care facilities won't accept patients with advantage plans because of the negotiated prices.

Either way you choose, it will cost you. In premium prices, or out of pocket.

They sure are. I haven’t found one yet that doesn’t get you somewhere. A lot of the plans tell you that you will get $40 or more a month for otc products, but how much Tylenol or band aids do you really need?None. Medicare Advantage Plans are a scam. I'll never leave original Medicare.

OneEyedDiva

SF VIP

- Location

- New Jersey

I will not be choosing any of them. I'm very satisfied with my state of N.J. retiree benefits insurance, which is Aetna PPO. I had Aetna HMO before getting on Medicare and the state seamlessly slid me into the Aetna HMO Medicare plan. Two years ago I changed to the PPO so that I won't have to pay extra should I need an out of network doctor.

My co-pays are $10 (except initial post surgery visits are free). I do not have to pay any hospital, surgery, lab or imaging bills. I do not have to deal with paperwork. 35 hours a week of at home care is covered for an unlimited time (I double checked this with a rep) and nursing home care is covered for 120 days per benefit period.

My co-pays are $10 (except initial post surgery visits are free). I do not have to pay any hospital, surgery, lab or imaging bills. I do not have to deal with paperwork. 35 hours a week of at home care is covered for an unlimited time (I double checked this with a rep) and nursing home care is covered for 120 days per benefit period.

One other issue with Advantage plans is that if you don't like it, switching back to traditional Medicare with a supplement may be an issue.

From Google:

When you switch to traditional Medicare, you may also want to consider purchasing a Medicare supplemental insurance policy, known as Medigap. Medigap policies help to pay your cost-sharing requirements under traditional Medicare. Depending on how long you have been enrolled in Medicare Advantage, Medigap insurers may not be required to sell you a policy unless you meet the medical underwriting requirements. You may want to contact a few Medigap insurers directly to see if you will be able to purchase a Medigap policy when you switch to traditional Medicare.

From Google:

When you switch to traditional Medicare, you may also want to consider purchasing a Medicare supplemental insurance policy, known as Medigap. Medigap policies help to pay your cost-sharing requirements under traditional Medicare. Depending on how long you have been enrolled in Medicare Advantage, Medigap insurers may not be required to sell you a policy unless you meet the medical underwriting requirements. You may want to contact a few Medigap insurers directly to see if you will be able to purchase a Medigap policy when you switch to traditional Medicare.

Aunt Bea

SF VIP

- Location

- Near Mount Pilot

I’m curious which letter medigap policy represents the best value for you and your situation.One other issue with Advantage plans is that if you don't like it, switching back to traditional Medicare with a supplement may be an issue.

From Google:

When you switch to traditional Medicare, you may also want to consider purchasing a Medicare supplemental insurance policy, known as Medigap. Medigap policies help to pay your cost-sharing requirements under traditional Medicare. Depending on how long you have been enrolled in Medicare Advantage, Medigap insurers may not be required to sell you a policy unless you meet the medical underwriting requirements. You may want to contact a few Medigap insurers directly to see if you will be able to purchase a Medigap policy when you switch to traditional Medicare.

My mother had a great medigap plan years ago through United Healthcare that paid for everything but I’m not sure that the twenty five years of premiums put her in a better place than a Medicare Advantage plan with some out of pocket expenses.

I live in a state that allows you to drop a Medicare Advantage Plan in favor of a medigap plan. If my health deteriorates I would consider making the switch during the annual enrollment period.

Vanessa2U

New Member

I looked into MediGap but it wasn't going to help me.I’m curious which letter medigap policy represents the best value for you and your situation.

My mother had a great medigap plan years ago through United Healthcare that paid for everything but I’m not sure that the twenty five years of premiums put her in a better place than a Medicare Advantage plan with some out of pocket expenses.

I live in a state that allows you to drop a Medicare Advantage Plan in favor of a medigap plan. If my health deteriorates I would consider making the switch during the annual enrollment period.

Pappy

Living the Dream

I have been with United Heathcare Advantage since I retired in 1999. Never had a problem with them and they had paid some huge bills for us. No co-pay charge for our regular doctor and $35 for specialist. Very happy with UHC.

Teacher Terry

Well-known Member

A plan g medigap pays after Medicare pays. Once your 240 deductible is paid per year you wouldn’t pay another dime. Can’t imagine how that doesn’t work.I looked into MediGap but it wasn't going to help me.

Aunt Bea

SF VIP

- Location

- Near Mount Pilot

In my area a Medigap Plan G monthly premium is approximately $150.00/month in addition to the $240.00 deductible.A plan g medigap pays after Medicare pays. Once your 240 deductible is paid per year you wouldn’t pay another dime. Can’t imagine how that doesn’t work.

At this point I come out ahead with a zero premium advantage plan.

If my health deteriorates it may make sense to switch to a plan G.

Insurance companies will deny you if you have pre-existing conditions!!If my health deteriorates it may make sense to switch to a plan G.

Knight

Well-known Member

Imogene

Senior Member

- Location

- Middle Tennessee

A lot of medical provides in my area won’t accept “Advantage” programs. What is accepted in my area can be vastly different one hour north.

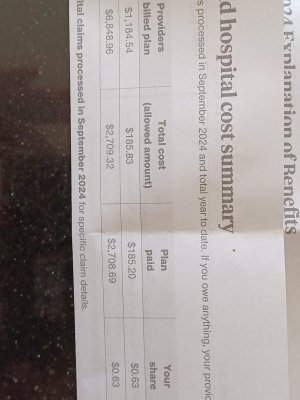

Husband and I had/h e BCBSTN. My passed in April from cancer. BCBSTN paid all but $1,700.00 to the hospital.

It is an expensive plan but they paid all but 4.6% of the hospital bill and paid 100% on the treatments at the cancer center for nearly three years.

I intend to keep my supplemental plan with them as it only takes one hospital stay to bankrupt a person.

Husband and I had/h e BCBSTN. My passed in April from cancer. BCBSTN paid all but $1,700.00 to the hospital.

It is an expensive plan but they paid all but 4.6% of the hospital bill and paid 100% on the treatments at the cancer center for nearly three years.

I intend to keep my supplemental plan with them as it only takes one hospital stay to bankrupt a person.

oldmontana

Senior Member

- Location

- Montana

I say it depends on the plan, where you live, and know if your providers are in network our out of network. We have been on Medicare Advantage with BC/BS for over 5 years and love it.None. Medicare Advantage Plans are a scam. I'll never leave original Medicare.

Did you know that to be on a Medicare advantage plan you have to be on Medicare?