Nice thing about TurboTax is that if you use the same computer year after year, the history of past years returns are automatically known to the TurboTax program for the current year. Sometimes the IRS wants you to enter information from previous years' taxes. That can be a pain to dig out from filed paperwork, but not for TurboTax. Also, capital gains carryforward losses are automatically remembered.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Do You Do Your Own Tax Return Or Pay Someone To Do It For You?

- Thread starter Lee

- Start date

jujube

SF VIP

I just did mine today. Easy-peasy.

SetWave

Well-known Member

- Location

- Monterey Bay

There's a group that does it for seniors which I used for a few years until now with the pandemic they will not meet face-to-face and it's more complicated than just doing it myself.

SetWave

Well-known Member

- Location

- Monterey Bay

I just did mine today. Easy-peasy.

Murrmurr

SF VIP

- Location

- Sacramento, California

I haven't filed a tax form since I had to go on SSI but someone told me that for the three years I had my foster son I was eligible for a refund so I went on TurboTax and filed for 2020. Then I went to file for 2019 and 2018, but apparently I should have amended the 2020 one instead. That got complicated so I went to H&R Block and the lady there said I already got all I was going to get. I didn't believe her, so I called the IRS.

A nice lady at the IRS went over the whole 3 years with me in about 15 minutes, and not more than a week later, well over $3000 went into my account.

A nice lady at the IRS went over the whole 3 years with me in about 15 minutes, and not more than a week later, well over $3000 went into my account.

Murrmurr

SF VIP

- Location

- Sacramento, California

Plus mine was -Back when I worked for a living, I did the short form;

1) What did you make last year

2) Send it in

Form: How many kids you got?

Me: 3.

Form: Name one ...and please affix a stamp.

I don't feel comfortable giving out my personal/financial info so I do my own even when I have to include additional forms for sold house or capital gain from investment. A few times I tried both the 1040 and the EZ forms to see which one give more refunds. It turned out that 1040 was the best for me even when my tax was simple. A couple decades earlier I volunteered at a computer warehouse to rebuild computers. One of the machines I worked on had lots of personal info including SSN, DOB, address and financial info in a database. It could be from an accounting office but they didn't wipe out the hard drive before donating it. As long as I can do it myself I'll continue doing it to stimulate my brain.

SetWave

Well-known Member

- Location

- Monterey Bay

Heard on the noon news that the deadline has been extended to 5/15. YAY!

horseless carriage

Well-known Member

We used to have a tax scheme known as MIRAS meaning mortgage interest relief at source. Instead of a tax rebate the mortgage payment was lower but it was scrapped in April 2000 by The Labour Party government's, Gordon Brown, who dubbed it a middle class perk.How about if you want to claim a tax rebate for interest costs on your mortgage or something like that? And how do pensioners do theirs?

The UK income tax system is known as PAYE or pay as you earn. We receive a form from the tax office on which we declare our income. The self employed will have a professional to do theirs but employed people just need to put down their employer, if they have one, and other sources of income. The tax office already know those sources because employers, pension funds and anyone who pays an income to someone has to declare it to their tax office.

An employee will get a tax code, and your tax threshold will be £12,500. That's how much you can earn tax free. After that we pay 20% on income £12,501 to £50,000 it the rises to 40% on income £50,001 to £150,000 and any income after that is taxed at 45%. If it interests you the UK tax office explains it in detail on their website. https://www.gov.uk/income-tax-rates

IrisSenior

Senior Member

- Location

- Ontario, Canada

I used to use H & R Block but a few years ago my daughter showed me how to use the Turbo Tax and now I do it myself.

tbeltrans

Senior Member

We go to a tax person. I figure the value by how long it would take me to figure it all out, consider the cost per hour at my current earning capacity when I do engineering contract work, and it turns out that the tax guy is a bargain by comparison. Whenever I am planning a purchase, whether it is somebody's labor as with the tax guy, or other goods or services, I figure it out by how many hours I am willing to work to purchase the thing. That usually makes these decisions very clear. I wouldn't go to one of those tax mills because they always seem to leave money on the table as another poster a bit earlier in this thread made abundantly clear, and my own experience in the past reflects similar results.

Tony

Tony

Robert59

Well-known Member

I'm glad to pay 30.00 dollars to have someone local do mine.

OneEyedDiva

SF VIP

- Location

- New Jersey

I started using H & R Block Tax Cut a decade or more ago. It provides the opportunity to e-file rather than dealing with all that paperwork The program is easy to use, it's efficient and for between $30 - $35 five people can use the program to file. My grandson uses my program and we split the cost. I've been satisfied. I use the print feature to generate PDF "copies" which I save in iDrive.com (not affiliated with Apple).

I have always done my own taxes on the paper form and mailed them in. I'm fully retired and my income is low and solely from interest, SS and pension so I fall below the level of having to pay federal tax and the need to file a form. I owe no tax to the state either, but they require me to submit a form anyway.

Last edited:

Kathleen’s Place

Senior Member

- Location

- Wisconsin

Turbo Tax for years now.

dobielvr

SF VIP

- Location

- California

I had to use them last year. Not happy about that.I go to H&R Block, they are expensive for even a simple return but it is quick and easy.

But today I went to my job sight to fill out some retirement ppwk, and I was able to do it there, for free.

Just have to go back and pick it up.

BTW...i just read somewhere that they're extending the deadline for filing till May.

***SetWave beat me to it ^^^^^

Last edited:

I used to use TaxAct-Online, but some years ago they made changes and it got hard to use and they were trying to charge money to use it, so I switched to Express1040.com. My daughter uses TurboTax, my mom used to have an accountant. My dad was very pro H&R but that's because he owned stock in it and did very well for him.

This year was a little hard because I sold a hay crop for the first time ever (which turned out to be "rent" income - which is what the kid that cut it told me, but I was hoping it would turn out to be 'farming' so I could get reduced property taxes, but oh well).

This year was a little hard because I sold a hay crop for the first time ever (which turned out to be "rent" income - which is what the kid that cut it told me, but I was hoping it would turn out to be 'farming' so I could get reduced property taxes, but oh well).

OneEyedDiva

SF VIP

- Location

- New Jersey

I never used the online version, never trusted it. Plus I had to use the Deluxe due to investments (also good for home and business owners). This is the first year I trusted to download the program. I usually buy the DVD but Amazon didn't have it available when I was ready to get started.I used to use TaxAct-Online, but some years ago they made changes and it got hard to use and they were trying to charge money to use it, so I switched to Express1040.com. My daughter uses TurboTax, my mom used to have an accountant. My dad was very pro H&R but that's because he owned stock in it and did very well for him.

This year was a little hard because I sold a hay crop for the first time ever (which turned out to be "rent" income - which is what the kid that cut it told me, but I was hoping it would turn out to be 'farming' so I could get reduced property taxes, but oh well).

Warrigal

SF VIP

- Location

- Sydney, Australia

In Australia we don't have state income tax and haven't since I was born. We do pay federal income tax. State revenue comes from allocations from the federal purse and from the Goods and Services Tax (GST). The states also levy stamp duty on property transactions, road tolls and other fees.

My income comes in the form of a part aged pension (means tested) from the Federal Government and from my allocated pension, which contains money contributed during my working life. Taxes were paid on money as it was invested so now that money is tax exempt. Income wise, with some concessions, I don't pay any income tax at all and have no need to submit a tax return anymore.

Before retirement we went to a local accountant because we had an investment property, now part of my allocated pension fund, and taxation law kept changing all the time. It was worth the money to engage the services of someone who kept up to date.

My income comes in the form of a part aged pension (means tested) from the Federal Government and from my allocated pension, which contains money contributed during my working life. Taxes were paid on money as it was invested so now that money is tax exempt. Income wise, with some concessions, I don't pay any income tax at all and have no need to submit a tax return anymore.

Before retirement we went to a local accountant because we had an investment property, now part of my allocated pension fund, and taxation law kept changing all the time. It was worth the money to engage the services of someone who kept up to date.

Thanks for the information. Sounds something like our system. We get a form with all that already filled in and just sign it and send it inWe used to have a tax scheme known as MIRAS meaning mortgage interest relief at source. Instead of a tax rebate the mortgage payment was lower but it was scrapped in April 2000 by The Labour Party government's, Gordon Brown, who dubbed it a middle class perk.

The UK income tax system is known as PAYE or pay as you earn. We receive a form from the tax office on which we declare our income. The self employed will have a professional to do theirs but employed people just need to put down their employer, if they have one, and other sources of income. The tax office already know those sources because employers, pension funds and anyone who pays an income to someone has to declare it to their tax office.

An employee will get a tax code, and your tax threshold will be £12,500. That's how much you can earn tax free. After that we pay 20% on income £12,501 to £50,000 it the rises to 40% on income £50,001 to £150,000 and any income after that is taxed at 45%. If it interests you the UK tax office explains it in detail on their website. https://www.gov.uk/income-tax-rates

Our income tax is local up to a certain income. After that limit we pay national but no local income tax on the excess.In Australia we don't have state income tax and haven't since I was born. We do pay federal income tax. State revenue comes from allocations from the federal purse and from the Goods and Services Tax (GST). The states also levy stamp duty on property transactions, road tolls and other fees.

My income comes in the form of a part aged pension (means tested) from the Federal Government and from my allocated pension, which contains money contributed during my working life. Taxes were paid on money as it was invested so now that money is tax exempt. Income wise, with some concessions, I don't pay any income tax at all and have no need to submit a tax return anymore.

Before retirement we went to a local accountant because we had an investment property, now part of my allocated pension fund, and taxation law kept changing all the time. It was worth the money to engage the services of someone who kept up to date.

Your pension is means tested? Here everyone gets a national pension no matter how much or little you earn. Then we have supplements that are paid in by your employer but the supplement isn't deducted from your salary. And of course you can take out a private pension insurance

Warrigal

SF VIP

- Location

- Sydney, Australia

The aged pension is means tested, taking into consideration both assets and income. The eligibility and pension payments depend on whichever test qualifies for the least payment. Hubby and I are assessed on the level of assets. The family home is exempt but all other assets are quantified and taken into consideration when determining payments.

Important: Your residential home is not included in the Age Pension assets test.

According to recent research by the ANU Centre for Social Research and Methods, 73% of households with at least one Age Pensioner are homeowners and 17.6% of these households have a home worth more than $1 million.

Any debts owing on assets other than your home is subtracted from their market value for the purposes of your assets test assessment. For example, if you have an investment property valued at $600,000 and you still owe $200,000 to the bank for the loan you obtained to buy it, the value of your investment property asset will be assessed at $400,000.

To be eligible for either a full or part pension, there are limits on the value of the assets you (and your partner combined) can own. The limits depend on whether you own your own home, as well as your living arrangements (including if you have a partner and whether they are age-eligible for the pension or not). The assets limits are higher for non-homeowners in recognition of the higher cost of housing for pensioners who rent their home.

Any debts owing on assets other than your home is subtracted from their market value for the purposes of your assets test assessment. For example, if you have an investment property valued at $600,000 and you still owe $200,000 to the bank for the loan you obtained to buy it, the value of your investment property asset will be assessed at $400,000.

To be eligible for either a full or part pension, there are limits on the value of the assets you (and your partner combined) can own. The limits depend on whether you own your own home, as well as your living arrangements (including if you have a partner and whether they are age-eligible for the pension or not). The assets limits are higher for non-homeowners in recognition of the higher cost of housing for pensioners who rent their home.

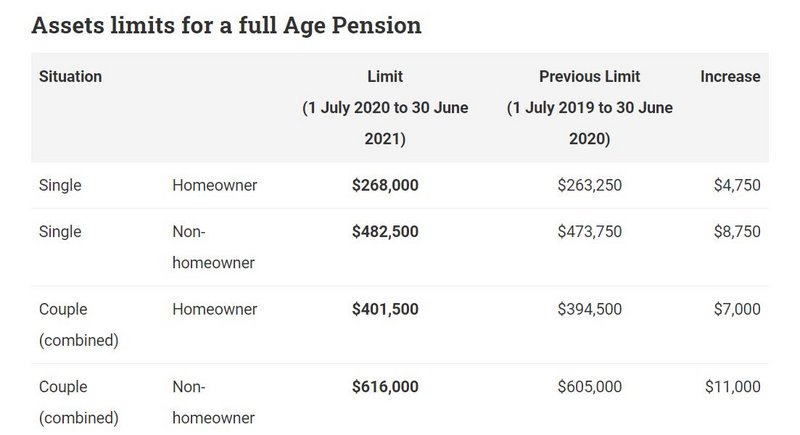

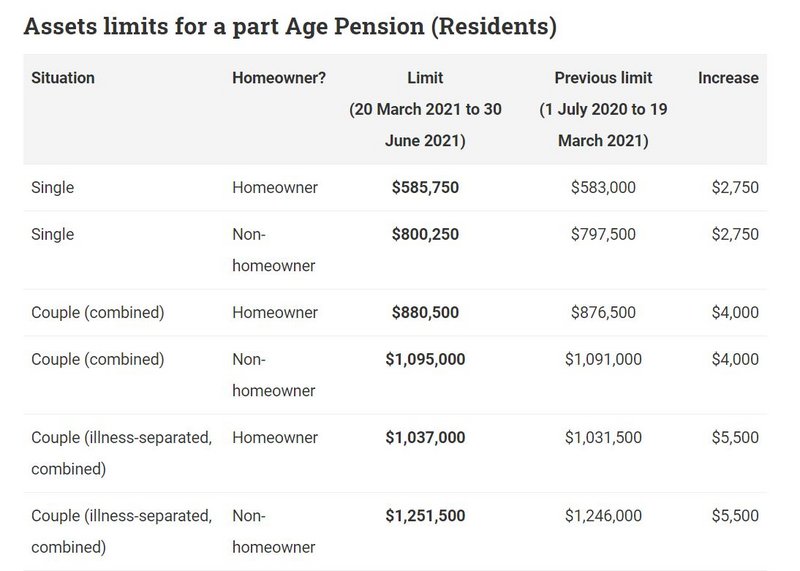

The current asset limits are itemised in the tables below. To be eligible for a full Age Pension the value of your assets must be below the following thresholds.

If the value of our assets is above the thresholds in the above table, you may still be eligible for a part Age Pension. The table below shows the maximum values of assets you can hold to still be eligible to receive any part pension payment.

The amount of Age Pension you are eligible for reduces by $3 per fortnight per $1000 of assets until it cuts off completely when the value of your assets exceeds the figures below.

Below is the table that applies to us.

We own our home and our combined assets, not including the value of our home, are less that A$880,500 so we are each eligible for a fortnightly government payment of $572.78 per fortnight. I have two other income streams from two allocated pension accounts that contain our savings. They are included in the assets test but the income from them is tax free. From the larger one I draw down $1,346.67 per month and from the smaller one A$402 per month. Hubby has similar income from his pension account. Between the means tested government payment (which is indexed every 6 months) and our own savings investments, we are quite comfortable. Currently all workers have about 9% on top of their wages paid into compulsory superannuation accounts by their employer that cannot be accessed until retirement age. By now, Australia has built up a very large level of savings that can be accessed in retirement and available for investment throughout our working lives. Withdrawal can occur earlier for hardship reasons.

How does the Age Pension assets test work? (in Australia)

The market value of any assets you or your partner own will be assessed by the Centrelink to determine your potential eligibility for the Age Pension.Important: Your residential home is not included in the Age Pension assets test.

According to recent research by the ANU Centre for Social Research and Methods, 73% of households with at least one Age Pensioner are homeowners and 17.6% of these households have a home worth more than $1 million.

Any debts owing on assets other than your home is subtracted from their market value for the purposes of your assets test assessment. For example, if you have an investment property valued at $600,000 and you still owe $200,000 to the bank for the loan you obtained to buy it, the value of your investment property asset will be assessed at $400,000.

To be eligible for either a full or part pension, there are limits on the value of the assets you (and your partner combined) can own. The limits depend on whether you own your own home, as well as your living arrangements (including if you have a partner and whether they are age-eligible for the pension or not). The assets limits are higher for non-homeowners in recognition of the higher cost of housing for pensioners who rent their home.

Any debts owing on assets other than your home is subtracted from their market value for the purposes of your assets test assessment. For example, if you have an investment property valued at $600,000 and you still owe $200,000 to the bank for the loan you obtained to buy it, the value of your investment property asset will be assessed at $400,000.

To be eligible for either a full or part pension, there are limits on the value of the assets you (and your partner combined) can own. The limits depend on whether you own your own home, as well as your living arrangements (including if you have a partner and whether they are age-eligible for the pension or not). The assets limits are higher for non-homeowners in recognition of the higher cost of housing for pensioners who rent their home.

The current asset limits are itemised in the tables below. To be eligible for a full Age Pension the value of your assets must be below the following thresholds.

If the value of our assets is above the thresholds in the above table, you may still be eligible for a part Age Pension. The table below shows the maximum values of assets you can hold to still be eligible to receive any part pension payment.

The amount of Age Pension you are eligible for reduces by $3 per fortnight per $1000 of assets until it cuts off completely when the value of your assets exceeds the figures below.

Below is the table that applies to us.

We own our home and our combined assets, not including the value of our home, are less that A$880,500 so we are each eligible for a fortnightly government payment of $572.78 per fortnight. I have two other income streams from two allocated pension accounts that contain our savings. They are included in the assets test but the income from them is tax free. From the larger one I draw down $1,346.67 per month and from the smaller one A$402 per month. Hubby has similar income from his pension account. Between the means tested government payment (which is indexed every 6 months) and our own savings investments, we are quite comfortable. Currently all workers have about 9% on top of their wages paid into compulsory superannuation accounts by their employer that cannot be accessed until retirement age. By now, Australia has built up a very large level of savings that can be accessed in retirement and available for investment throughout our working lives. Withdrawal can occur earlier for hardship reasons.

|

Butterfly

SF VIP

- Location

- Albuquerque, New Mexico USA

After a very unpleasant run-in with the IRS about 40 years ago (which I finally won, but had to hire a tax attorney to do so), I swore I would never again do my own tax return. It's a promise I've kept. Running afoul of the IRS is an experience you'll never forget.

funsearcher!

Member

Went to a free tax clinic at the senior center this year--they take your info one week and have someone do the taxes and 2 people check it then you come back to sign the next week. Zero cost and it is DONE.